Extracting mineral resources in Ukraine during and after the end of the war with EU support and investments from foreign partners

Ukraine is one of the richest countries in minerals and critical raw materials, which play a significant role in international trade and global production processes. The country has a unique mineral resource base, with around 20,000 deposits and occurrences of 117 types of mineral resources identified. Of these, 8,172 deposits containing 94 types of minerals hold industrial significance.

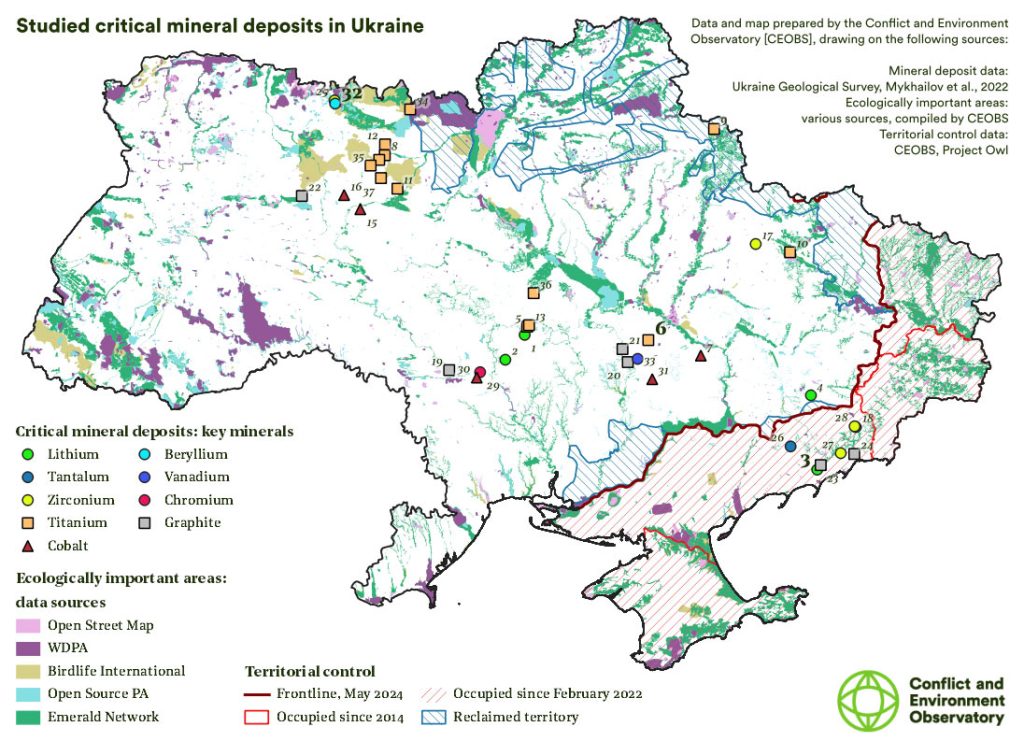

Due to Russia’s full-scale invasion that began in 2022, a significant share of Ukraine’s mineral resource base has been affected by occupation. According to consolidated Ukrainian and international estimates, approximately 40% of Ukraine’s mineral resources are located in territories currently under Russian occupation, including parts of the Donetsk, Luhansk, Zaporizhzhia, and Kherson oblasts. These areas contain important deposits of coal, iron ore, lithium, titanium, and other critical raw materials.

According to Forbes Ukraine (2023), the total estimated value of Ukraine’s mineral resources exceeds $15 trillion, with a substantial concentration in the eastern and southeastern regions of the country.

On the territory controlled by Ukraine, mineral resources remain with an estimated value of about $4.5 trillion. However, the exact valuation of rare earth metals in these areas is difficult due to limited access and insufficient exploration of deposits.

Ukraine holds 21 out of 30 substances that the European Union (EU) classifies as “critical raw materials”, accounting for about 5% of global reserves, making the country attractive to investors.

Many territories where these elements are located lie in the southern part of the Ukrainian Crystalline Shield, mainly under the Sea of Azov. Most of these areas are currently occupied by Russia; however, Ukraine still has promising projects in the Middle Pobuzhzhia region, as well as in Kyiv, Vinnytsia, and Zhytomyr regions.

According to experts, although several hundred promising geological sites have been identified in Ukraine, only some of them can be turned into mining projects if their development is deemed economically viable.

Ukraine possesses significant deposits of critical minerals, including:

- Lithium – confirmed reserves account for about one-third of all European reserves (around 3% of global reserves);

- Graphite – Ukraine ranks among the world’s top five countries in terms of reserves;

- Titanium – Ukraine is among the world’s top ten producers, and the deposit in Zhytomyr region (Stremigorod) is one of the largest on the planet;

- Uranium – Ukraine holds the largest reserves in Europe and ranks 11th worldwide.

In addition, the country has significant reserves of other strategically important metals, such as manganese, iron, gold, lead, zinc, cobalt, nickel, copper, zirconium, and others.

Uranium, titanium, and graphite have been mined in Ukraine for many years, while lithium mining projects remain at the planning stage. Additional geological exploration could help assess and expand the country’s prospective resources.

Ukraine also has reserves of 17 rare earth elements. The most significant include: Cerium (Ce), Lanthanum (La), Neodymium (Nd), Samarium (Sm), Yttrium (Y), Gadolinium (Gd), Dysprosium (Dy).

The main rare earth deposits are:

- Mazurivske (Zhytomyr region) – one of the largest in terms of ore reserves;

- Azov (Donetsk region) – significant titanium and zirconium deposits;

- Kirovohrad region – rich in uranium and rare earth metals;

- Volyn deposit – promising area for geological exploration.

The considerable reserves of rare earth resources in Ukraine are of special interest to today’s global market, especially the EU and the US.

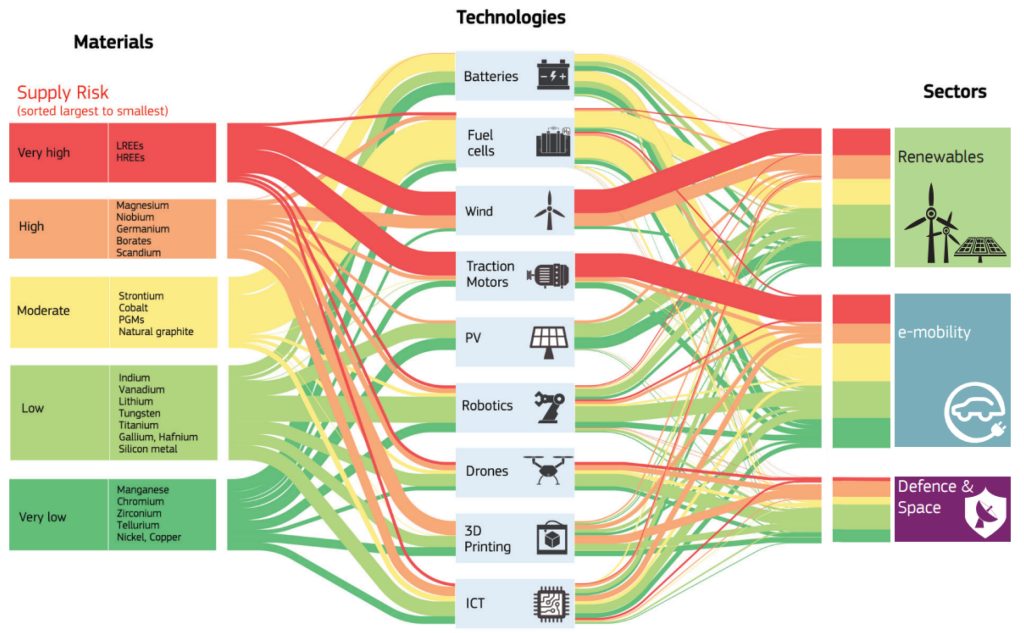

In the modern global economy, natural resources, particularly critical and rare earth elements, play a key role in the development of highly industrialised, high-tech countries, as they are indispensable for producing modern electronics, renewable energy technologies (wind turbines, electric vehicles), aerospace, military equipment, navigation systems, and advanced industrial technologies, including artificial intelligence data centres.

Without these elements – despite their “rarity” in terms of concentration and the difficulty of extraction – it is impossible to produce high-tech products. Natural resources, especially rare earth metals, are essential for advanced countries to sustain economic growth and maintain their leadership in the global economy. Their use enables technological leadership, competitiveness, and the development of high-tech industries, ensuring the production of innovative products and supporting strategic sectors.

Currently, China dominates the global rare earth market, controlling over 60% of production and about 85% of processing. In 2022, China produced around 210,000 tons of rare earth elements, far exceeding other countries. This creates a strategic dependence of many nations on Chinese supplies.

China’s monopoly in this field is explained by several factors: significant reserves, state support for mining and processing, and strict export quotas. In recent years, the US, EU, and other governments have actively sought alternative sources to reduce dependence on China, opening opportunities for new players, including Ukraine.

Ukraine has promising rare earth deposits, but their development requires significant investment and technological support. Ukraine’s rare earth reserves are estimated at millions of tons, though industrial-scale mining has not yet started. Potential partners include the European Union and the US, who are actively seeking alternative supply sources, since much of Europe’s industry depends on imports from China. Ukraine can become a strategic partner in diversification programmes for raw material supplies.

Rare earth metals could play a key role in Ukraine’s economic development and provide a powerful boost to the economy. If the country succeeds in attracting large-scale investment and introducing modern extraction technologies, it could become an important global player in the rare earth market.

Ukraine is ready to grant access to its resources and create a favourable investment climate for capital from the EU, US, and other foreign partners on a mutually beneficial basis, using advanced processing technologies. However, successful cooperation requires consideration of geopolitical risks, transparent agreements, and long-term guarantees.

Ukraine stands on the threshold of a rare earth breakthrough, and it is important to manage this resource effectively. The country needs a clear strategy for developing rare earths that considers investment, technology, and geopolitical risks. The main directions of this strategy could include:

- Attracting investors and international partners

Developing rare earth mining requires major capital. Ukraine can attract investment from Western partners, including the EU, US, and Canada, who are interested in diversifying supplies of critical minerals. - Developing infrastructure and technologies

To efficiently mine and process rare earths, Ukraine needs modern facilities, including:

Ore beneficiation plants capable of processing ores rich in rare earth elements;

Research centres developing innovative methods for processing and extracting metals;

- Government support and regulation

Legislative initiatives are needed to stimulate the development of the rare earth sector, including tax incentives for investors, simplified licensing procedures, and protection of strategic deposits from external influence. - Geopolitical protection and security of deposits

Given the current situation, special attention should be paid to the security of strategically important deposits. Control over them is a key factor for Ukraine’s economic stability and energy independence.

Rare earth metals can become a powerful driver of Ukraine’s economic growth, but only if extraction and processing policies are well-structured. Effective resource management would allow Ukraine not only to strengthen its economy but also to secure an important place in the global supply system of critical metals.

Vital minerals of strategic importance for the EU

Ukraine’s significant mineral resources are crucial for the EU’s digital and green transition:

- Titanium: Europe holds the world’s largest reserves, about 7% of global stocks.

- Lithium: One of Europe’s largest deposits, around 500,000 tons.

- Graphite: Ukraine supplies around 20% of global supply.

- Beryllium, gallium, uranium, zirconium, apatite, and fluorite are examples of rare earths critical for defence, aerospace, and semiconductors.

- Cobalt and nickel: Found in secure areas such as Kirovohrad and Dnipropetrovsk.

In total, Ukraine possesses 22 out of 34 raw materials classified as critical by the EU, and about 5% of global reserves of critical raw materials.

The EU and other international partners would greatly benefit from investing in Ukraine’s mineral sector. With its huge reserves of critical raw materials, Ukraine has strong potential to contribute to the EU’s strategic autonomy and green transition.

To launch such investment projects, both Ukraine and its international partners must first establish a strong legal framework. This begins with comprehensive agreements and alignment of strategies through coordinated policy integration.

The first step lies with the Ukrainian government, which must prioritise developing modern infrastructure, facilitating access to mining projects, and creating a transparent regulatory environment. Offering tax incentives and investment support mechanisms will also be key to attracting responsible foreign investors.

On the other hand, the EU can provide significant support to its companies investing in Ukraine. This includes political backing, war risk insurance, and investment protection tools to ensure long-term security and confidence for European businesses in the region.

With coordinated efforts, international investment in Ukraine’s mineral sector could bring mutual benefits, enhancing economic resilience, strengthening partnerships, and supporting sustainable development for both Ukraine and the EU.

Before launching investment projects, EU member states must conduct a comprehensive SWOT analysis and carefully assess market conditions, investment attractiveness, potential risks, competitive environment, as well as the political and geological context both regionally and nationally.

SWOT analysis for EU-supported investment projects

| Strengths | Potential to create robust supply chains, alignment with the EU’s Critical Raw Materials Act, and a large strategic resource base. |

| Weaknesses | Out-of-date geological data, limited refining capacity, and ongoing war. |

| Opportunities | Expanding Ukraine’s refining capabilities, diversifying EU supply chains, and cooperating within EU frameworks. |

| Threats | Geopolitical instability, China’s hegemony in refining, legal ambiguity, and reputational hazards. |

The Background and Consequences of the US-Ukraine Minerals Agreement

The Ukraine-United States Mineral Resources Agreement, which was signed in April 2025, established a Reconstruction Investment Fund and stipulated that Ukraine would pay 50% of future profits from government-owned natural resources, such as lithium, titanium, uranium, oil, natural gas, and rare earth elements.

This deal raises concerns about sovereignty and EU accession alignment, even though it seeks to reduce Western dependence on China and guarantees sustained US involvement. Crucially, the agreement does not give US companies exclusive rights, which allows European projects to play a big role, particularly in safer areas and in the development of refined infrastructure.

Businesses and investment projects in Europe – interest is already being reflected in tangible actions

German industry associations, such as VDMA and BGR, are advocating for German companies to be involved in the development of Ukraine’s mineral value chains.

A number of Austrian and Central European businesses are considering joint ventures in the extraction of titanium and graphite; the European Commission has designated Ukraine a priority partner within the Critical Raw Materials Club (2024), creating opportunities for collaborative projects; and the Polish Development Bank (BGK) has launched financing instruments specifically designed for critical raw material projects in Ukraine.

It is anticipated that European and international investors will participate in Ukraine’s August 2025 tender for the development of a lithium deposit in Kirovohrad oblast (Reuters).

Investment landscape of Ukraine’s mineral regions

| Region | Key minerals | Category | Investment attractiveness | Risk | Competition | Why attractive |

| Kryvyi Rih, Nikopol | Iron, Manganese | Traditional | ≥ 70% (High) | ≤ 30% (Low) | High | Established infrastructure, high reserves, budget contributions |

| Zhytomyr Region | Titanium, Zirconium, Hafnium, Quartz, Piezoquartz, Feldspar, Building Stones | Traditional / Highly Promising | ≥ 70% (High) | ≤ 30% (Low) | Medium–High | Rich in strategic and industrial minerals, developed transport, high demand |

| Kirovohrad Region | Uranium, Graphite, Scandium, Garnet, Rare Earths | Traditional / Highly Promising | ≥ 70% (High) | ≤ 30% (Low) | Medium–High | Strategic and battery minerals, active exploration, energy relevance |

| Dnipropetrovsk Region | Titanium, Lithium, Foundry Sands, Refractory Clays | Traditional / Highly Promising | ≥ 70% (High) | ≤ 30% (Low) | High | Mining hub, active operations, stable demand |

| Donetsk Region | Foundry Sands, Rare Earths, Building Stones | Traditional / Highly Promising | ≥ 70% (High) | ≤ 30% (Low) | Medium | Industrial use, proximity to production facilities |

| Lviv, Ivano-Frankivsk Region | Potassium Salts, Flux Limestones | Highly Promising / Promising | ≥ 70% / 50–69% | ≤ 30% / 31–50% | Medium | Fertilizer production, constant demand |

| Zaporizhia Region | Rare Earths, Niobium, Tantalum, Chromium | Highly Promising / Promising | ≥ 70% / 50–69% | ≤ 30% / 31–50% | Medium–Low | Tech-critical raw materials, underdeveloped fields |

| Vinnytsia Region | Kaolin | Traditional | ≥ 70% (High) | ≤ 30% (Low) | High | Stable market in ceramics and construction |

| Kharkiv Region | Scandium, Garnet | Highly Promising | ≥ 70% (High) | ≤ 30% (Low) | Medium | Niche strategic minerals |

| Khmelnytskyi, Chernivtsi | Feldspar, Stone-Coloured Raw Materials | Promising | 50–69% (Medium) | 31–50% (Medium) | Low | Industrial minerals for construction and ceramics |

| Other / Scattered Regions | Vanadium, Zinc, Fluorite, Beryllium, Gold, Boron, Glauconite, etc. (with unclear potential) | Unclear Prospects | < 50% (Low) | > 50% (High) | None | Localized deposits, low certainty and undeveloped infrastructure |

Sources: Gaylin, A.M., Rudko, G.I., Chikova, I.V. (2017) Mining-Chemical Potential of Ukraine and Investment Atlas of Subsurface User: Strategic and Critical Minerals (2021). Available here.

The European Union’s role

{kind=link}

By 2030, 10% of annual consumption should come from EU extraction, 40% from processing, and 25% from recycling, according to the EU’s ambitious Critical Raw Materials Act (2024). Ukraine’s resource base directly supports these goals by offering diversification away from China and Russia. Through EU funding mechanisms, political support, and risk insurance, European investors can secure essential supply chains and contribute significantly to Ukraine’s reconstruction.

Conclusions

Ukraine’s mineral wealth presents a strategic opportunity that is both immediate and long-term:

1. To get the most out of the deal for both sides, Ukraine needs to update its laws, rules, and infrastructure.

2. The EU should promote ethical investments by making licensing more open and offering war-risk insurance.

3. European businesses should focus on value-added processing in Ukraine instead of just raw extraction.

4. Initial focus should remain on stable oblasts like Zhytomyr, Kirovohrad, and Vinnytsia.

Strategic collaboration in Ukraine’s resource sector will strengthen the EU’s resilience, support Ukraine’s economy, and forge a lasting partnership for Europe’s green transition.

LATEST

What does it mean to be part of the European family?

Ukraine as the foundation of new European security: from integration to EU strategic autonomy

Reflections from the 2026 European Forum for Young Leaders

Lost Ukrainian Atlantis: the flooded memory of Polina Raiko’s house

Why does Armenia’s future belong to the youth who defend it?

The information on this site is subject to a Disclaimer and Protection of personal data. © European Union,